On March 9, Stanford Law students heckled and shouted down a 5th Circuit Judge who was giving a talk hosted by the school’s student chapter of the Federalist Society. Among the grievances of the heavily progressive student body was that the judge had refused to use, in a 2020 opinion, the preferred pronouns of a transgender person who had been convicted of several offenses related to child pornography. (“In conjunction with his appeal, Varner also moves that he be addressed with female pronouns. We will deny that motion.”)

The judge was reportedly unable to complete his prepared remarks, and during question time was subjected to invective, such as the question, “I fuck men, I can find the prostate. Why can’t you find the clit?”

Apparently, when one of the school’s diversity deans arrived to “restore order,” she ended up criticizing the judge, while other administrators failed to tell protesting students to allow the judge to speak without being interrupted.

Student members of the Federalist Society were further subjected to a name and shame campaign, and allegedly “encircled” and abused at the event after federal marshals escorted the judge away.

The judge later remarked, “Don’t feel sorry for me. I’m a life-tenured federal judge. What outrages me is that these kids are being treated like dog shit by fellow students and administrators.”

On March 11, the Dean of the law school, Jenny Martinez, and the University President, Marc Tessier-Lavigne, sent a written apology to the judge:

We are very clear with our students that, given our commitment to free expression, if there are speakers they disagree with, they are welcome to exercise their right to protest but not to disrupt the proceedings. Our disruption policy states that students are not allowed to “prevent the effective carrying out” of a “public event” whether by heckling or other forms of interruption.

In addition, staff members who should have enforced university policies failed to do so, and instead intervened in inappropriate ways that are not aligned with the university’s commitment to free speech.

Dean Martinez followed that up with an email to alumni clarifying the law school’s stance on free speech.

In response to the apology, “hundreds of student protestors wearing masks and all-black clothing lined the hallways outside Stanford Law School Dean Jenny Martinez’s classroom” where she was teaching a con law class. She “arrived to find her whiteboard covered in fliers ridiculing Duncan and defending those who disrupted his speech. The fliers echoed the opinion of student activists and some administrators who claimed hecklers derailing Duncan’s talk was a form of free speech.”

“They gave us weird looks if we didn’t wear black” and join the crowd, first-year law student Luke Schumacher said. “It didn’t feel like the inclusive, belonging atmosphere that the DEI office claims to be creating.”

As a law school alumnus, I found this behavior incredibly embarrassing.

You only have to flip the roles to highlight how ridiculous it is. What if it were a left-leaning circuit judge being yelled at and insulted by a motivated group of right-leaning students? Would the same progressive students who yelled down Judge Duncan support the right’s right to do so then? I doubt it.

I am not familiar with the judge’s jurisprudence, but to be clear, with respect to the viewpoints of his that were reported by the media, I do not agree with them. But that should not matter here.

I can’t think of any other country which has a more expansive right to free speech than the U.S., and it is a fundamental enough right that it is enshrined in the constitution. However, if you seek to wield that right, you wield a double-edged sword. The same right that allows anyone to speak out on political topics without fear of government prosecution, allows other people to picket (at a distance) the funerals of gay murder victims with hate speech. But that is kind of the point. As a result, censorship is something that runs contrary to free speech values, and not letting someone talk by shouting over them en masse is a form of censorship. And, at some point, that kind of disruption can cross the line into unlawful speech—harassment, threats, slander, and the like.

Stanford is a private university and is not legally required to uphold free speech values. However, these values share much in common with the notion of academic freedom, and so it is unsurprising when Dean Martinez writes, “Freedom of speech is a bedrock principle for our community at SLS, the university, and our democratic society. … The way the event with Judge Duncan unfolded was not aligned with our institutional commitment to freedom of speech.”

It’s not clear in the reporting whether the protesters were law school students, or students from other parts of the university (events like these are normally open to all to attend). If they are law school students, what are they going to do when they become lawyers and get in front of a judge they disagree vehemently with, but still need to present a case to?

(Sidenote: Interestingly, unlike the U.S., a few countries like England and Australia, practice the “cab-rank rule” which obliges barristers to accept work from any client as long as they are competent enough to handle it, and regardless of any personal distaste the barrister may have for their client’s reputation, character, etc. “Without the cab-rank rule, an unpopular person might not get legal representation; barristers who acted for them might be criticized for doing so.” So in these countries, you not only need to have the ability to present a case respectfully in front of a judge you may personally hate, but you may also need to do it on behalf of a client you find repugnant. Not easy but, in my opinion, an important part of the justice system.)

Further Observations

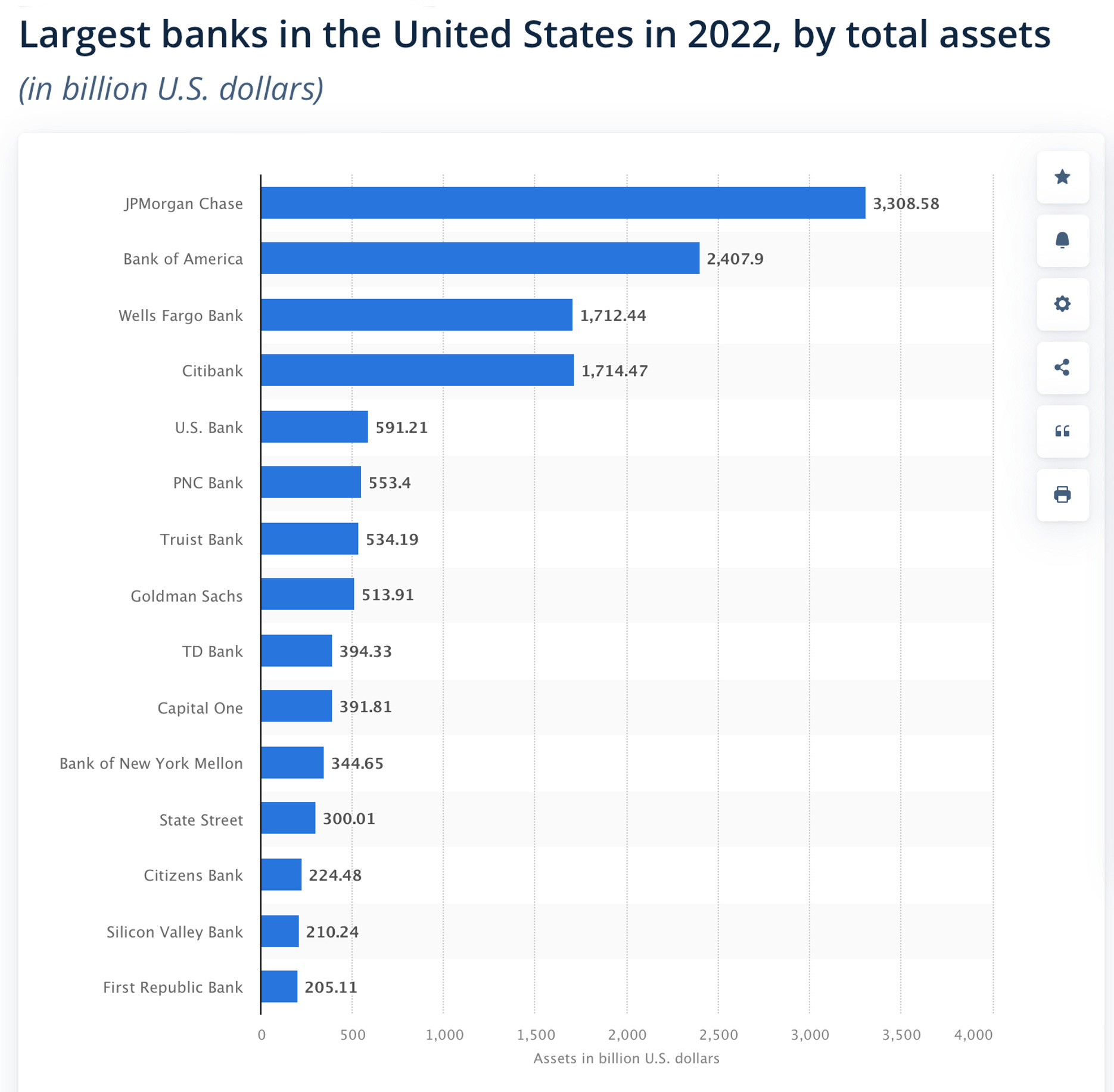

Last week’s newsletter about SVB produced the highest number of views out of all my past newsletters. The drama continued this week, with regional banks under pressure. One of the most notable among these banks is First Republic, a San Francisco-based bank that serves a lot of high net worth individuals. First Republic has been experiencing an outflow of deposits which has led to efforts to shore up its balance sheet. In addition to obtaining a $70 billion credit line, a consortium of large banks deposited $30 billion on Thursday. First Republic was reportedly also looking for an acquiror. However, those efforts failed to calm the markets, and the stock closed down for the week, reflecting skepticism that First Republic will be able to weather the storm without going into receivership.

On the other side of the Atlantic, UBS has agreed to buy Credit Suisse for about $3.2 billion in an all stock deal which is expected to close by the end of this year. That’s 0.50 Swiss francs per share, which is about a quarter of CS’ stock price at market close on Friday.

Everything Everywhere All at Once won seven Oscars last Sunday. Unusually, EEAAO took out most of the top shelf awards, including Best Picture, Best Director, and three acting awards, despite being a sci-fi flick. Also unusual was that two Asians from the movie landed two of the acting awards: Michelle Yeoh won Best Actress in a Leading Role, and Ke Huy Quan won Best Actor in a Supporting Role. (Jamie Lee Curtis landed the award for Best Actress in a Supporting Role.) Yeoh is the first Asian winner of her award in Oscars history. Harrison Ford presented the awards, which was a nice touch seeing that Ke Huy Quan last appeared on screen with him in Temple of Doom as Short Round. EEAAO is an absurdist film that I found difficult to follow at times, but it’s quite a spectacle with some memorable scenes, including one featuring butt plugs which people are doing their best to sit on.

Strong winds caused another power outage at our home on Tuesday. It lasted 12 hours for us, but 48 hours for our kids’ preschool. Due to the recent rains saturating the ground, a lot of large trees were uprooted, leading to widespread blackouts throughout the Bay Area. We had to spend a night at a hotel again.

In other news, Tesla has finally started selling its Powerwall on a standalone basis again. Due to supply constraints over the last couple of years, Tesla would only sell Powerwalls bundled with solar panels. The recent blackouts have pushed us towards buying a pair.

Never Split the Difference (Chris Voss) A very interesting book written by a former hostage negotiator for the FBI. It highlights the shortcomings of a more traditional “principled” approach to negotiation, where rationality rules the day, and focuses more on the emotional and human aspects of negotiation. Voss asserts that compromising (”splitting the difference”) is a cheap way out that often leads to sub-optimal results for both parties. Sometimes there’s a way to get all of what you want, even when it appears you have little or no leverage, and without blowing up the relationship.

Hotels

Residence Inn by Marriott San Mateo – San Francisco Airport (San Mateo) Unfortunately, the nearer (and nicer) Residence Inn we stayed at during the last power outage was all booked out. This hotel is older, but still pretty well equipped and pretty good to work from. We got upgraded to a two bedroom, two bathroom suite split over two levels.

Charts, Images & Videos

On Twitter

Danger! Workers are doing too well! Call the Fed to shut that down! A conversation with former Treasury Secretary Larry Summers. Watch the full interview in our latest episode, now streaming on @appletvplus. pic.twitter.com/B6GtO0QLnw

— The Problem With Jon Stewart (@TheProblem) March 17, 2023

You guys know what happened to the stock market the last two times this happened? pic.twitter.com/j0GvICdBB6

1/10 The USG response has likely stemmed contagion. However, $SIVB saga has effectively forced the mkt to price the entire Fed Funds rate into the funding cost of the regional banking system. An acceleration in lending contraction is here.

Silicon Valley Bank is, relatively speaking, just down the road from me. As one the top 20 largest banks in the U.S., it is the banker to half of the startup industry but, fortuitously, not to my employer.

At the start of this week, SVB held about $170 billion of deposits from its customers. On Thursday, it fell victim to a bank run. SVB’s customers, within the space of about 24 hours, withdrew $40 billion—a quarter of its deposit book. This is a tremendous amount, and SVB did not have enough cash on hand. In fact, at the end of the day, it had a cash shortfall of almost $1 billion dollars. When a company is unable to pay its debts as and when they fall due (and on Thursday, $40 billion suddenly fell due), the company is considered insolvent and cannot continue business as usual.

On Friday, SVB was placed into receivership. A federal government agency called the Federal Deposit Insurance Corporation (FDIC), took over management of SVB and immediately closed it for business. Anyone still with money in SVB was now unable to get it out. “Anyone” turns out to be mostly startups, who are now facing an uncertain and very stressful few days.

But how did we end up here? Why did customers suddenly want to pull out $40 billion? And if took in $160 billion in deposits, why did they have not enough cash to pay $40 billion back?

What happened?

We don’t normally think about things in this way, but a deposit in a regular bank account is basically a loan to the bank that you can ask the bank to repay at any time (which essentially happens when you go to an ATM and withdraw cash, or ask Venmo to send money from your bank account to a friend). In exchange for lending money to the bank, they pay you interest (normally). Banks use your money to make money. Typically, this is done by lending those deposits to other people, at higher interest rates. So, for example, you might lend the bank $100,000 and they pay you 1% interest, but then someone else might borrow that $100,000 from the bank to buy a house (i.e. a mortgage loan) and pay the bank 3% interest. They pocket the 2% difference.

But the loans that banks make aren’t “on demand”. If you have a 30 year mortgage, you only need to repay a certain amount, plus interest, each month. The bank normally can’t force you to pay more than that. On the other hand, the money you lend to the bank in a regular savings account is “on demand”. This is sometimes referred to as “borrow short and lend long” and is just how banks work.

So, given that timing mismatch, how can the bank lend any money out? After all, it’s no good if you go to the bank one day and want your $100,000 back, only to be told “sorry, we lent your money to someone else and we have to wait 30 years before we get it all back”.

Enter “fractional reserve banking”. In reality, people rarely ask for all their money back at once, and never does everyone ask for all their money back at once, so banks only need to hold back a fraction of their deposits as cash, and can lend the rest of it out (or invest it in other things that are expected to produce a positive return). The fraction that banks need to hold in reserve is fittingly called the reserve requirement, and is set by banking regulations.

There are situations in which unusually high amounts of withdrawals may exhaust a bank’s reserves, but there are usually also facilities available under which banks can borrow money (typically from other banks) on a short-term basis to fill any holes while they scramble to convert their other assets (loans and investments) back to cash.

SVB was in a slightly different situation, but the basic principles are the same. The main difference is that their client base is heavily composed of tech startups. Most tech startups are not profitable or cash flow positive, so they finance their operations by raising equity financing (giving up a piece of the company in exchange for money), rather than debt financing (paying interest in exchange for money). Missing an interest payment on a loan can be deleterious, so when you’re not reliably making money as a startup, debt can be dangerous and is usually avoided. As a result, SVB didn’t have a lot of avenues for lending out the money it had received from its customers to other customers, so it needed to find another place to invest that money to earn a return.

For this, SVB invested a lot in debt in the form of U.S. treasury bonds and mortgage backed securities. When you buy a U.S. treasury bond, you are lending the U.S. government money, and they pay you interest. Treasuries are considered “risk free” in the sense that the U.S. government will always be able to pay you back. They can do this because they can just print money, if they need to. (Let’s leave to one side for now the game of chicken that politicians play every few years with the debt limit.) So from a creditworthiness perspective, treasuries are a very conservative investment vehicle. They are also a very liquid asset, which means there is a deep and active market that lets you buy and sell a lot of bonds quickly.

Because the short-term interest rates have been near zero for so long, SVB decided to invest in $90 billion worth of longer-term bonds that returned a little less than 2% of interest per year, and the full amount of principal after several years.

During the pandemic years, investment in tech startups blossomed, with equity financing pouring into companies at ever increasing valuations. Consequently, because of how concentrated SVB’s client base is in tech startups, their deposits trebled from about $60B at the start of 2020 to almost $200B just a couple years later.

In 2022, after over a decade of near-zero interest rates, rates began rising sharply, to around 5% today. SVB started to find itself having to pay more interest on its deposits, increasing the need for SVB to earn a return on all that money that its customers had lent it. However, most of its money was locked up in those long-term bonds, which was one problem.

The other problem, is that due to increasing rates, the funding environment for startups tightened right up—instead of investing in startups, more people were now investing in treasuries, which were yielding more than they had for over a decade (and remember, treasuries, unlike startup investments, are considered risk free). On the other hand, tech company valuations were getting slashed. This meant that as startups spent their money, no new funding was coming in to replace it. SVB’s deposits started to fall by billions of dollars as startups withdrew money to pay employees and vendors.

SVB needed to start converting some of its investments back to cash so that it could pay those customer withdrawals. Here’s where the problem started.

Most of SVB’s assets were treasuries. If those treasuries are held to maturity, SVB gets all its money back. But if it needs the money now, SVB needs to sell those treasuries now. Unfortunately, if SVB paid $100 for a treasury bond that only pays $2 in interest a year, no one today is going to buy that bond for $100 because the U.S. government is currently issuing bonds that pay $5 in interest. So if SVB sells those bonds, they are going to have to sell them for something less than $100.

This was a problem for SVB, because let’s say it sold some bonds for 95% of what they bought them for. Accounting rules require SVB to consider that its entire bond portfolio is now only worth 95% of its original value. For a $90 billion portfolio, that’s a $4.5 billion decrease. In reality, it’s reported that the bond portfolio had actually lost $15 billion in value. So if they sold some of those bonds, they would have a massive $15 billion hole in their assets that they’d have to plug somehow (remember, that’s $15 billion they no longer have to cover the deposits they’ve taken in). So those bonds were effectively untouchable in the short term.

Instead, SVB sold substantially all of its other investments for cash—$21 billion worth—it also tapped out some other lines of credit it had. As a forced seller, it incurred a $1.8 billion loss on the sale because those investments had declined in value. To plug that hole, SVB tried to do what all of its startup clients do—raise $1.75 billion equity financing. In the press release for the equity raise, the $1.8 billion dollar loss is mentioned in the last paragraph, almost as an afterthought.

People noticed, and this news spooked people. People started to wonder why SVB decided to liquidate $21 billion at a significant loss, and rumors started to fly about whether SVB was in trouble.

Bank Run

Silicon Valley is a pretty interconnected community and news spreads fast. For example, my CEO was plugged into his CEO and VC network and hearing what was going down. Our head of finance was talking to other heads of finance at peer companies. I was reading buzz from a mailing list with hundreds of head of legal on it. Word started circulating that companies were getting their money out of SVB, just in case. It became an echo chamber.

The other thing about having tech startups as clients is that they are tech experts, not finance experts. A large number of tech startups are run by talented under-35 founders who have not experienced a financial crisis in their professional lives, nor are they finance experts. As a result, they logically turned to their VCs for advice on what to do when the rumors started. After all, VCs are “the money guys” and they should know much more about financial management since that’s the industry they effectively operate in. So when one VC says “get your money out,” that causes a whole bunch of their portfolio companies to do just that.

Having seen how fast things unravelled in 2008 (“Bear Stearns is fine!”), my initial reaction to hearing the news was: Get your money out of SVB right fuckingNOW… if you can. As in, drop whatever you’re doing and get those wire instructions in. If it’s nothing, you can always move the money back.

If you didn’t have a second bank account, or you had a loan with SVB that contractually required you to keep your cash with them, things got a bit trickier, and you then had to make calls like whether to move the cash into a founder’s personal bank account, or ignore your loan covenants, and then worry about any legal ramifications afterwards.

The next morning, and $40 billion in withdrawal requests later, SVB was dead. The FDIC announced that SVB was both insolvent and failing its regulatory liquidity requirements.

There has been some blowback against some VCs for fanning the flames of a bank run that might have been avoidable, but I don’t think VCs are to blame here. As a company, you have to look out for your own employees and business and, in this case, taking your money out if you could was the right call. If it’s a false alarm, there’s little downside. But if it’s real, then you don’t want to be stuck in a tough place… especially if it was avoidable. The herd mentality is a powerful driver of financial markets and you want to at least be part of the stampede—not be crushed by it.

What now?

Through the FDIC, the U.S. government provides deposit insurance at all FDIC-insured banks. If a bank collapses, the FDIC will ensure that depositors will be able to get at least $250,000 of their funds back. (This limit used to be $100,000 but was raised after 2008 Great Financial Crisis.) This is very helpful for the average person, who is likely to have less than $250,000 cash lying around in a bank account. It is not so helpful for a company, that is likely to have much more than that. Apparently, about 96% of SVB depositors were not fully covered by FDIC insurance, compared to about 38% at Bank of America.

This insurance kicks in very quickly. On Friday, the FDIC created a new bank called the Deposit Insurance National Bank of Santa Clara (DINB). The insured portion of all SVB bank accounts was then transferred to the new bank, and depositors will have access to those new bank accounts on Monday. The uninsured portion of those bank accounts (anything over $250K per depositor) was then effectively frozen, with the FDIC issuing a “receivership certificate” to each depositor that represents an unsecured claim on the remaining assets of SVB up to the amount of the uninsured funds.

Next, the FDIC’s job will be to sell off SVB in a way that maximizes the money they receive. That money is then distributed to a list of people, starting with secured creditors, then depositors, then other unsecured creditors, then subordinated debt holders, then anything remaining goes to SVB’s stockholders.

As the FDIC sells off SVB, it will issue a dividend to receivership certificate holders. It’s rumored that the FDIC has been hard at work flogging off tens of billions of dollars’ worth of SVB’s assets and will issue an “advance dividend” of about 50% of the value of a certificate sometime in the next week.

The best outcome now is for another bank with a strong enough balance sheet to buy SVB and assume all the deposits in one fell swoop, which will allow accounts to be unfrozen. I think that is a likely outcome. If that doesn’t happen, then SVB will be sold off in pieces, and uninsured depositors will get their money back over time. I think that depositors will get most, if not all, of their money back, but it will take months, or even years.

In the meantime, the timing uncertainty and inability to access funds is incredibly stressful to affected startups. Payroll is due next week. Failure to pay wages is one of the things that can “pierce the corporate veil”, meaning that liability for that failure spills beyond the company, and may impact officers, directors and stockholders personally. However, one would think that if employees get paid a few days late, they’re going to be understanding and not litigious.

This weekend, startups are trying to find sources of immediate-term funding, ranging from loans from VCs, bridge loans, credit cards, and selling their receivership claims at a discount to opportunistic investors.

And teams of bankers, lawyers, and bureaucrats are spending a sleepless weekend trying to figure out what to do with SVB before the markets open on Monday.

I think the majority of SVB startups will be fine at the end of the day. There may be a severe liquidity issue for startups with short runways (e.g. if you had a 12 month runway and only get 50% of your funds back next week, you now have a 6 month runway and no idea when the remainder of the money will come back, and you’re now thinking about whether you need to lay off people to conserve cash).

[UPDATE: It’s over; startups can feel relief. 30 minutes before this post was scheduled to go out: ‘The Federal Reserve, Treasury and Federal Deposit Insurance Corporation announced in a joint statement that “depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.” The agencies also said that they would enact a “similar systemic risk exception for Signature Bank,” which the government disclosed was closed on Sunday by its state chartering authority.’ (per the New York Times) “Separately, the Federal Reserve announced that it was creating a new lending facility for the nation’s banks, designed to buttress them against financial risks caused by Friday’s collapse of SVB.” (per the Washington Post).]

Bail outs?

Several prominent VCs and investors have been screaming for the federal government to come in and backstop deposits in full—not just $250K. In other words, the government should effectively insure everything, and then get reimbursed as FDIC sells off SVB.

This is not a bailout of SVB. SVB is no more—its board and executive team will find themselves looking for new employment (if not already), and the equity holders will likely be wiped out.

But it is a bailout of depositors, and that has other people screaming that the U.S. taxpayer should not have to do that either. Let capitalism take its course. (And, as usual, the whole situation has been politicized.)

The issue is more nuanced than that. As I mentioned above, although depositing money at a bank is essentially lending the bank money (and therefore a form of investment), people don’t really see it like that. And you’re not really thinking that the 16th largest bank in the U.S., which has been around for 40 years and is regulated, is a credit risk. The average person on the street certainly isn’t going to be thinking about that. They’re just looking for a place to put money that isn’t under their mattress. During my time in the U.S., I have had personal bank accounts at a lot of different financial institutions (more than half a dozen), and creditworthiness was never something that crossed my mind.

So is it fair or desirable that depositors should suffer—particularly when what we are talking about here are small innovative businesses that employ thousands of people between them?

But then should we just make FDIC insurance unlimited for everyone going forward? If not, why not?

Some suggest that a failure by the government to backstop depositors here will catalyze a chain reaction that leads to catastrophic bank runs at other (small) banks. The argument goes that why would anyone put money in a smaller bank that is at risk of a bank run? People will just move money into the biggest 4 banks in the U.S., which will cause further bank runs, kill small banks, and lead to more concentration and less competition in the banking industry, which is bad for everyone. I’m not very convinced by this argument. I think we are in a specific situation exacerbated by the uniquely concentrated customer base that SVB had (only 3% retail clients!) which produced a high proportion of uninsured deposits.

This was also a liquidity issue, not a situation where SVB plowed billions into FTX stock that is now worthless and they now can’t cover the hole. SVB apparently has enough assets to cover its deposit liabilities—it just needs time to sell them off. People probably aren’t going to lose a lot of money, unlike when your crypto exchange goes belly up.

As for the question why anyone will now deposit in small banks if there’s no backstop—in most banks, the existing backstop covers most depositors. Secondly, why do people bank with smaller banks today? Because their product is positively differentiated in various ways. I’m skeptical that the perception of a potential threat of a bank run happening to a smaller bank is going to outweigh all the other reasons that smaller banks exist in a way that leads to an existential crisis for them. But let’s see what happens when the markets open on Monday.

Another thing that is clear to me is that we now have a generation of workers who have been exposed to a financial crisis for the first time. To be sure, it’s mostly localized to tech startups (for now), but for almost 15 years now, money has been cheap and free-flowing and the last 9 months have been a huge shock to the system. It will be intriguing to see how these interesting times shape the psyche of Gen Z and younger millennials, just like how the financial habits of the Silent Generation were shaped for a lifetime after growing up through the Great Depression.

More to come

I still think the worst is yet to come for the economy as a whole. If interest rates are sustained at current levels (and it’s starting to look that way, as employment is still strong and inflation remains elevated), we’ll start to see them bite into the parts of the economy that are the most sensitive to rate rises, and that will cause a domino effect. I’m not sure where that is, but I could see, for example, companies that have maturing loans getting into trouble when they have to refinance at much higher market rates. Or unrealized losses that bondholders being forced to be realized due to liquidity needs.

If you spend much time on AI twitter, you might have seen this tentacle monster hanging around. But what is it, and what does it have to do with ChatGPT?

It's kind of a long story. But it's worth it! It even ends with cake 🍰

The failure of @SVB_Financial could destroy an important long-term driver of the economy as VC-backed companies rely on SVB for loans and holding their operating cash. If private capital can’t provide a solution, a highly dilutive gov’t preferred bailout should be considered.

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank. Absent @jpmorgan@citi or… https://t.co/SqdkFK7Fld

Warren Buffett’s annual shareholder letter was published as part of Berkshire Hathaway’s annual report last week. This year’s was quite brief, but as usual, very accessible and a repeated reminder of the simple themes that have served him well over the decades.

After the growthy period of 2019-2021, Berkshire returned to outperforming the S&P index, returning 4.0% in a year where the market fell 18.1%.

“We are understanding about business mistakes; our tolerance for personal misconduct is zero.”

Berkshire buys businesses and also invests in public companies with the expectation of holding each indefinitely and therefore looks for enduring businesses with trustworthy managers. He notes that private, controlled businesses are almost never available at bargain valuations.

He notes that they make, on average, one “truly good” decision every 5 years, and that the performance of their portfolio of businesses includes “a large group that are marginal” but many that are “very good” and a few that are “truly extraordinary”.

For example, he highlights the performance of a 28-year holding of Coca-Cola. Cost base was $1.3B. As of 2022, it threw of $704M in cash dividends (53% annual yield on the original investment!) with a market value of $25B (19x capital gain).Put another way, if my parents had invested $100k in Coke when I was in primary school, that investment would today be almost $2M and generating $53k in dividends. Makes me think about what I should do for my kids to leverage the power of compounding. They are each currently, as Morgan Housel puts it, “time billionaires”.

Last year, Berkshire acquired another property-casualty insurer, growing its insurance float from $147B to $164M (the premiums it holds).

Berkshire holds a “boatload of cash and U.S. Treasury bills” and avoids behavior that could result in uncomfortable cash needs at inconvenient times, including financial panics and unprecedented insurance losses. Seems like a good personal approach too.

He rails against the politicization of stock buybacks. As a pure matter of mathematics, stock buybacks, when performed at a good (undervalued) price, are beneficial to all remaining shareholders.

His formula: retaining earnings in its businesses (Berkshire doesn’t pay dividends) + compounding + avoiding major mistakes + what he calls the American Tailwind: “America would have done fine withour Berkshire. The reverse is not true.”

Berkshire’s annual corporate tax bill of $31B is 0.1% of the entire American tax base.

He shares a bullet point list of some things Charlie Munger said on a podcast, including the value of being a patient, long-term investor, the dangers of leverage in wealth destruction, that you “don’t need to own a lot of things to get rich”, and that investing requires adapting as the world changes.

In reference to Charlie Munger: “Find a very smart high-grade partner — preferably slightly older than you — and then listen very carefully to what he says.”

Phones at Work

When I was younger, I generally disliked talking on the phone (there was a measure of anxiety attached to it), so the advent of SMS, emails, and IMs felt like a blessing to me, and more so as the younger generations pushed adoption of that socially, and then in the workplace. However, especially in tech workplaces, I now find myself missing phone calls.

To contact someone now, people typically reach out via Slack and then wait. Or schedule some time on their calendar and then wait. Or if it’s really urgent, they’ll send a text and then wait. It’s less intrusive, but also there’s no way to guarantee a quick answer for small things — even if the person is completely available, they just might not see your message for a while. And for a lot of these calls you simply don’t need video. You just need to get some shit done.

When I was a junior lawyer at a firm, we had these Cisco IP phones on our desk. People would just dial each other up by punching in 4 digit extensions. It was spontaneous, marvelously tactile, and it wasn’t a big deal. If the other person was unavailable (in a meeting, on another call, or just under the gun getting something out), they would ignore the call or send it to voicemail. (And if it was super urgent and you weren’t answering, they would physically show up at your door.) No one really worried about interrupting anyone. Clients would call out of the blue as well.

For a period I had an office next door to my supervising partner (I still remember his 4-digit extension, 15 years on), and he would still call me despite the physical proximity. I was thankful that he didn’t scream through the wall, even though that would have been marginally quicker.

These calls were a great way to deal with things in a minute that can now take quite a lot of minutes and relative effort to resolve over chat. Also, it’s a great way to ask a bunch of questions in a way that feels natural but, when done over a textual medium, can feel interrogational and even aggressive.

No one does this anymore, and I think you lose a valuable communication method and tool.

Further Observations

This week I learned that the U.S. Supreme Court opens each term with the pronouncement “Oyez, oyez, oyez!” Oyez is an Anglo-Norman word that means “Hear Ye!” It’s kind of weird that it took me so long to learn that given that I work in law and also started a blog called Hear Ye! over 20 years ago.

A 15-lawyer Canadian litigation law firm tried the 4-day work week for 2 years and published its results (Wednesday was their off day). They are pragmatic and interesting:

“Sometimes you’d have to work 5, 6, or 7 days a week and that is OK; that’s just life.” In other words, at a normal law firm you sometimes have to work weekends. In this case, the weekend is 3 days long, and you may have to work weekends. Particularly since clients expect availability and the courts have their own schedules. “In my interviews with our lawyers, they said they have had to work at least 1 hour or more on over 50% of Wednesdays.”

“You can attract the wrong crowd by advertising 4-day work weeks and need to get your message right and clear.” They put in a 3 month probationary period that requires new hires to work 5 days in the office until they get an idea of their work ethic.

“We have way, way less turnover.” This makes sense. And this suggests people chuck sickies quite often: “Our sick day requests have been reduced by over 80%.”

They still managed to grow revenue over that period (more than 2x over 2 years).

Drive to Survive (Season 5) “It’s not a documentary. It’s closer to Top Gun than a documentary.” —Toto Wolff. Great way to whet the appetite for the new F1 season, which started this week!

There's an easy way to measure Google's moral temperature at any given time: how closely the ads resemble the search results. pic.twitter.com/QZ15aOa0Ak

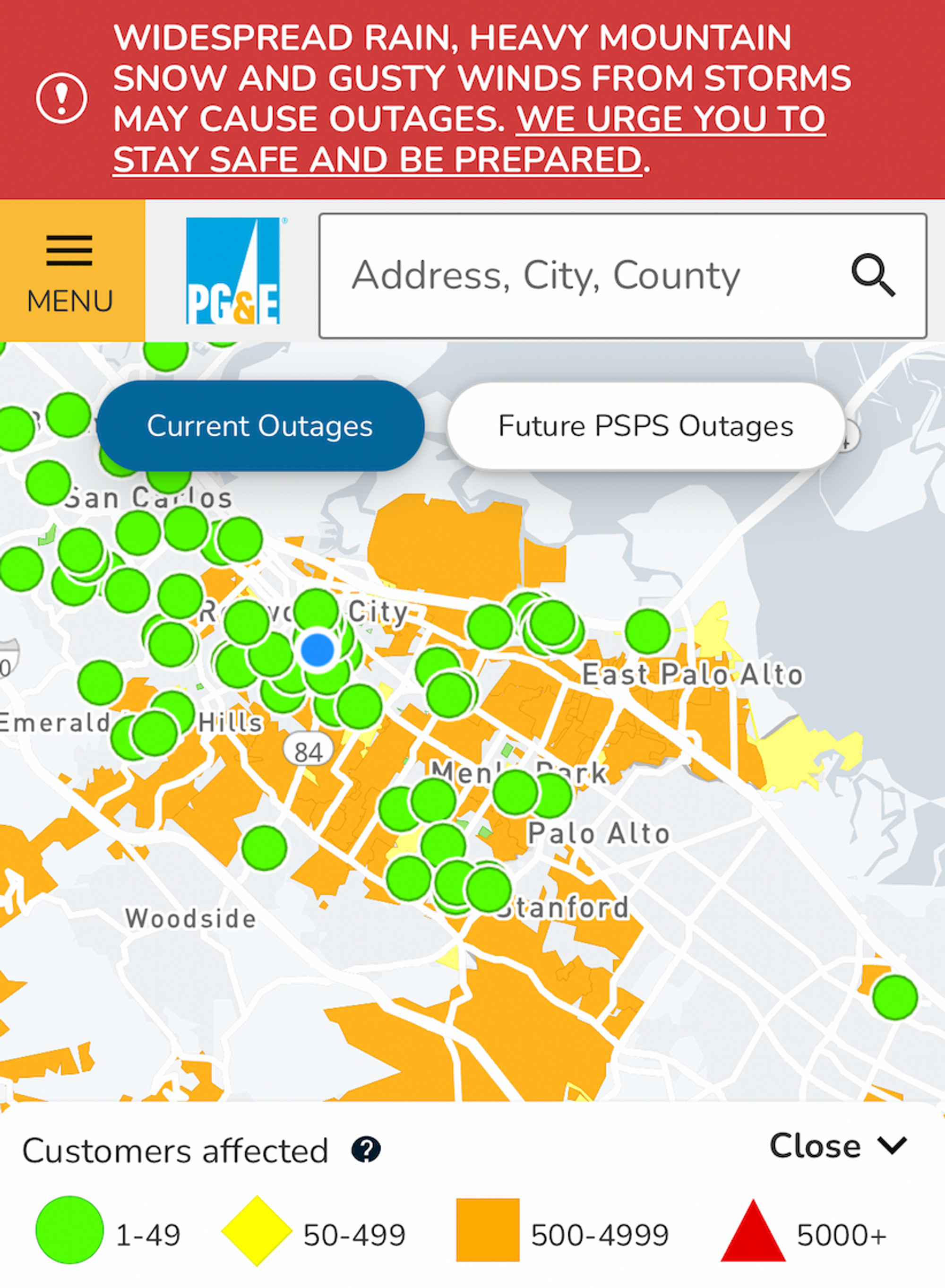

In a previous newsletter, I mentioned we have a lengthy power outage on average once per quarter. That’s not an exaggeration. This week, we endured our longest outage yet.

At about 1pm on Tuesday, our power went out and didn’t come back until Thursday evening — more than 50 hours later. It all happened as unusual weather arrived in Bay Area, with several inches of snow falling at altitudes of as low as 250 feet. It basically never snows in the Bay Area. Less than 5 miles away in Woodside, the scene looked like this:

Stephen Lam/The Chronicle

We didn’t get snow, but our area was buffeted by gale force winds that uprooted large trees, crushing power lines and transformers.

Within a few hours, power was out across swathes of Redwood City, Woodside, Atherton, Menlo Park, Palo Alto, East Palo Alto, and Stanford.

We ended up staying in hotels for 3 nights. The hotels were filled with locals — mostly families with young children and older people carting along oxygen containers.

At the first hotel, a Holiday Inn, we were offered a welcome bag of snacks at check in. “The robot will deliver them to your door,” the guy at the counter said, pointing to what looked like a trash can on wheels in the corner. I won’t lie — it was the most Silicon Valley thing ever, and I was more excited about it than was rational.

Some time after we got settled into the room, we got a call from the front desk. “The robot is outside your door.” I opened the door and there sat the robot. It did nothing. The screen on top of the robot featured two blinking eyes, with a speech bubble above in which was written “None.”

We stared at each other for a bit. After poking and prodding at the thing, I finally determined it wasn’t working, and called up the front desk. They fiddled with a few things on their end to no avail.

“We’re going to reset it and try again.”

Reset meant that someone had to come up to our room and manually wheel the robot back to its base. A few minutes later, the robot showed up at our door again. The result was not different.

“Again?!” an exasperated voice from the front desk said after I called them. And once again, they had to “reset” the robot.

Finally, the front desk clerk showed up at our door, his arms overflowing with snacks and beverages. “Sorry about that — we’re having uh, technical issues. I got you some extra things.”

Gradually, the power started to come back on in various places. We noticed that power in the most affluent areas was restored first — Atherton, Woodside, Palo Alto — while Redwood City and East Palo Alto were out of luck for hours longer. Maybe a coincidence, but we have our suspicions.

The most annoying part of the outage was all the food we had to throw out from our fridge and freezer.

The Rewriting of Roald

I entered Year 3 as a 7 year old, and some of the classroom memories I retained from that year include:

My teacher read to us The Hobbit and The Lion, The Witch and The Wardrobe, which was the first time I was exposed to fantasy and set in motion a lifelong affinity for that genre.

He read to us The Great Piratical Rumbustification and proceeded to put the last three words of that title on the next week’s spelling test.

He read to us Charlie and the Chocolate Factory, my first Roald Dahl book. During the course of primary school, I followed up by reading most of the rest of his novels, as well as his autobiographical Boy and Going Solo.

He was telling us about what to bring to an excursion to the mangroves of the newly-opened Bicentennial Park and mentioned we should bring “several drinks”. I thought that meant seven drinks, which seemed like quite a lot to me. I put my hand up. “Sir, do we have to bring several drinks?” He looked confused and said, “Well, you don’t need to but I would recommend you do.” I was satisfied that I wouldn’t get into trouble if I didn’t bring seven poppers and it was not until much later that I learned what “several” really meant.

In hindsight, many of those memories involved books, which brings us to the topic of Roald Dahl. Dahl is best known for his children’s novels, although he also had a repetoire of adult writing. His books were formative to me growing up. Last week, it was reported that Dahl’s books would be rewritten to remove language “now deemed too offensive”.

The laundry list of changes includes describing Augustus Gloop as “enormous” instead of “fat” (?!), removing many instances of “white” and “black” as descriptors in non-racial contexts (such as where you might describe a “face going white” for when the blood drains from the face in fright), and excising any mention of Joseph Conrad or Rudyard Kipling and replacing them with Jane Austen and John Steinbeck. One can only surmise that the associations of Conrad and Kipling with colonialism have been deemed too painful to tolerate.

The changes are reminiscent of a “Harmful Language” list that was published by a group within Stanford University. As that list would have it, words like “brave”, “tribe”, “abort”, “stupid”, “victim”, “immigration”, “submit” and “American” were considered harmful. The list was widely pilloried, and the university swiftly had it removed.

Online, it would appear that the changes to Dahl’s books are facing a similar backlash. This Reddit post is basically filled with people who are screaming “nobody asked for this”. In fact, one of the only negative comments I came across online was a one-star review that someone left 4 years ago for a 16-book collection of Dahl’s writings sold by Costco: “I bought this excited to read Charlie and the Chocolate Factory and the rest of the books with my kids. Then we got into the Great Glass Elevator, which has a chapter devoted to totally worn out racist tropes that made me stop reading.”

They’re not wrong about the racist tropes. Check out this passage from Great Glass Elevator:

The President threw the phone across the room at the Postmaster General. It hit him in the stomach. ‘What’s the matter with this thing?’ shouted the President. ‘It is very difficult to phone people in China, Mr President,’ said the Postmaster General. ‘The country’s so full of Wings and Wongs, every time you wing you get the wong number.’ ‘You’re not kidding,’ said the President.

…

The President again picked up the receiver. ‘Gleetings, honourable Mr Plesident,’ said a soft faraway voice. ‘Here is Assistant-Plemier Chu-On-Dat speaking. How can I do for you?’ ‘Knock-Knock.’ said the President. ‘Who der?’ ‘Ginger.’ ‘Ginger who?’ ‘Ginger yourself much when you fell off the Great Wall of China?’ said the President. ‘Okay, Chu-On-Dat. Let me speak to Premier How-Yu-Bin.’ ‘Much regret Plemier How-Yu-Bin not here just this second, Mr. Plesident.’ ‘Where is he?’ ‘He outside mending a puncture on his bicycle.’ ‘Oh no he isn’t,’ said the President. ‘You can’t fool me, you crafty old mandarin!’

It just goes on and on, doesn’t it?

As a child of the 80s of oriental persuasion, I am acutely aware of racism and being bullied in the playground for how my eyes looked as a “fucking ching chong chinaman”.

But I don’t think rewriting old works is the right thing to do. This is the progressive equivalent of censorship, and not much better than the troubling wave of book banning in more conservative parts of America.

History can be a great teacher, and only if you are aware of what happened in the past can you learn from it. Changing Dahl’s words is kind of like attempting to avoid history because it’s too painful, and seems similar in vein to avoiding teaching about the Holocaust in school.

Older books are products of their times and make good discussion points. I think it’s better that a child stumbles across the phrase “queer ramshackle house”, gets confused, and asks an adult how a house can be gay. That can spark a useful conversation.

It doesn’t seem much different to studying Shakespeare, where there are a lot of confusing, archaic words and phrases that high school students spend hours scratching their heads over. And I’m not sure that reading Shakespeare perpetuates the use of those dated terms.

I am far more fearful about what my kids will find online, than in a book from centuries past. I am more fearful about what text-generative AI might mean for critical thought and disinformation.

The other thing is, and this is perhaps controversial, is that there is a time and a place for ethnic stereotypes, and that is comedy. There’s a reason why Russell Peters’ jokes about Chinese and Indians (and everyone else) are so hilarious, and that we find Colin Jost reading out Michael Che’s jokes about black people funny. That comedy is only funny if you’re aware about those stereotypes in the first place.

I think the approach taken by Warner Bros. is the right one. For some of their older cartoons, they now display the following disclaimer at the start:

The cartoons you are about to see are products of their time. They may depict some of the ethnic and racial prejudices that were commonplace in American society. These depictions were wrong then and are wrong today. While the following does not represent the Warner Bros. view of today’s society, these cartoons are being presented as they were originally created, because to do otherwise would be the same as claiming these prejudices never existed.

Black Panther: Wakanda Forever (Disney+) I fell asleep midway through, so not that great. The first one was better. 2/5.

Only Murders in the Building (Season 2) This whodunnit series, featuring the unusual but endearing combination of Steve Martin, Martin Short, and Selena Gomez has really grown on us this season. It’s got a really random brand of humor that we like. We’re looking forward to Season 3, which is going to feature Meryl Streep and Paul Rudd. 4/5.

Hotels

Holiday Inn Redwood City (Redwood City, CA) Where we stayed for the first night. A standard, no frills hotel room. Clean and relatively comfortable.

Residence Inn Redwood City (San Carlos, CA) This place was surprisingly good, and actually a great place to stay if you are a business traveler. All rooms have a kitchen, two large tables, and are clean, spacious, and well appointed. There’s also a laundry on site. The breakfast is not bad.

On Twitter

THE banker of China IT industry. Fan and I started our careers about the same time. He was working for Morgan Stanley when we first met. We have been friends over 2 decades and watched the growth of each other https://t.co/47bn8mloWT

Put another way: nearly entire population of CA will be able to see snow from some vantage point later this week if they look in the right direction (i.e., toward the highest hills in vicinity). Snow remains very unlikely in CA's major cities, but it'll fall quite nearby. #CAwxhttps://t.co/m4PNoBtl0z

A Financial Times article reporting on the final days of FTX featured the following email that a partner from Sullivan & Cromwell, the law firm managing FTX’s bankruptcy proceedings, sent to SBF in an effort to get him to sign documents where he’d step down as CEO of FTX and allow FTX to file for bankruptcy.

EMAIL – NOV 10, 22:36 FROM: ANDY DIETDERICH TO: SAM BANKMAN-FRIED Can we please have an update? We have many people in NY and Delaware waiting to proceed. We have done the work we can without Sam’s signature. If Sam is not going to sign the instruction appointing Ray tonight, we will send people home and regroup in the morning. Australia has commenced voluntary proceedings and we can expect more shortly. If Sam is signing relatively promptly, we can stay around. Please let us know promptly if we should continue to wait. Andy

We now have learned just how “many people” from SullCrom were working on the matter and standing by. Per Coindesk: During a 19 day period from November 12 to 30, “A total of over 6,500 hours were worked by 32 partners, 85 associates and 34 nonlegal staff, the filing said. Hourly rates are as high as $2,165. The company said charges for senior staff already represent a discount, and the firm is seeking payment of only 80% of a $9.5 million total.”

The GC of FTX US is an ex-SullCrom partner, and while it may look a bit shady that he has given a ton of lucrative work to buddies at his old firm, this is actually an above-board and common practice for ex-law firm lawyers who go in-house (I have done this myself… but obviously not on this scale).

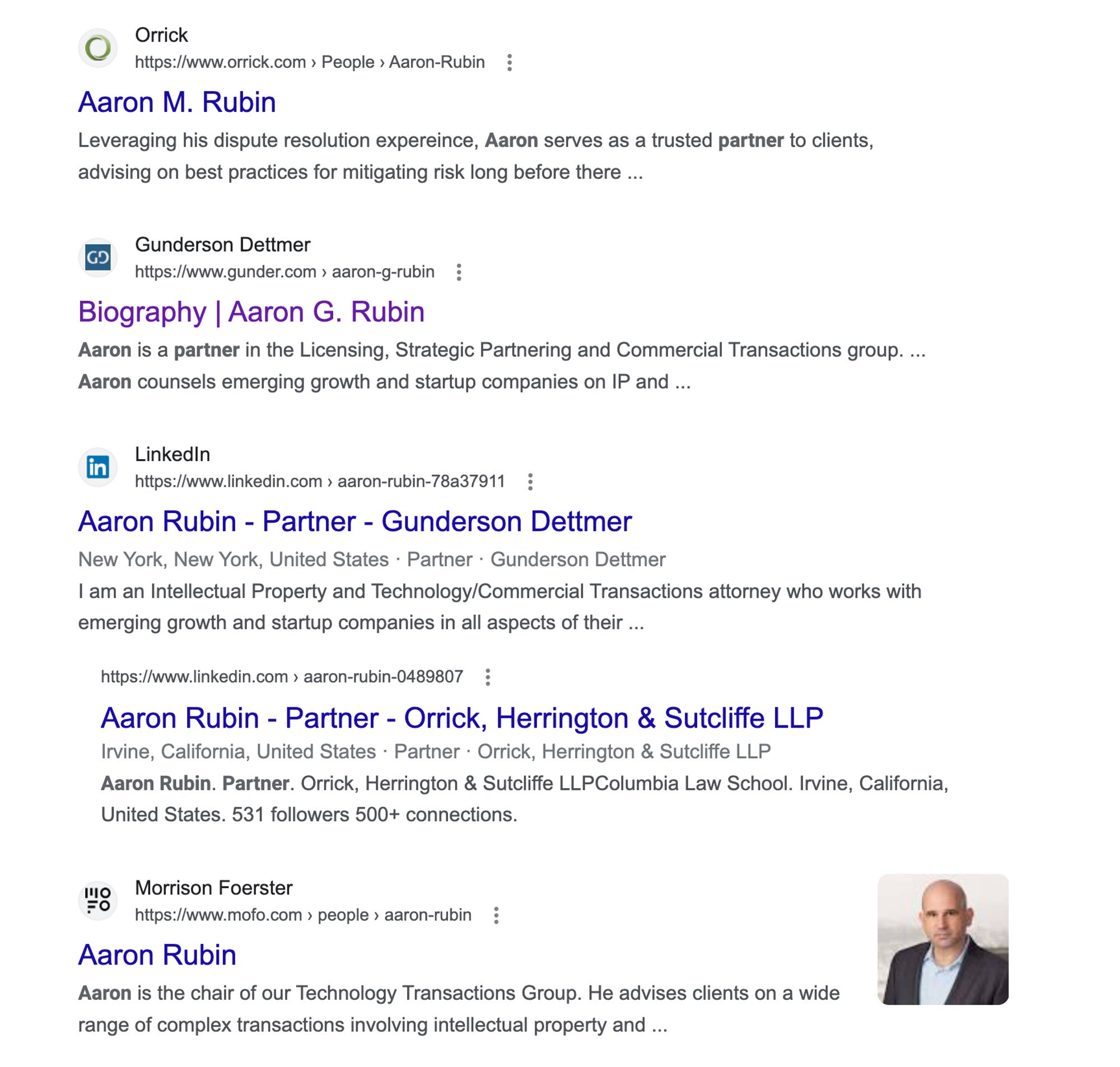

If you want to your son to be a partner at a Bay Area-headquartered law firm, you should name him Aaron Rubin:

In the 3 months after my son turned 2, his vocabulary exploded. He went from a smattering of single words to speaking 5-word sentences seemingly overnight. I found myself wondering whether the trajectory of our daughter’s speaking skills was as steep, but it’s actually really hard to remember. We thought it wasn’t, but when we pulled out videos, it turns out that she was pretty talkative at that age too. The takeaway is: take lots of videos of your children, including of random, seemingly inane moments.

The next generation of kids will be the first generation that will be able to see pictures of what their parents looked like during every single month of their lives. That’s kind of wild. My kids will only be able to see pictures of how I looked like every month of my life since my mid-20s, which I’m thankful for.

I have a recommended reading list for Artificial Intelligence, and it hasn't changed since 2019. I give this list to my grad students, but all of the articles are broadly accessible if you're interested. Very short 🧵.

Today @SECGov charged Kraken for the unregistered offer & sale of securities thru its staking-as-a-service program.

Whether it’s through staking-as-a-service, lending, or other means, crypto intermediaries must provide the proper disclosures & safeguards required by our laws.

Mostly random personal updates this week. Always so much work and so many household chores to catch up on after coming back from a vacation.

Air Travel Tips

Here are some international travel habits that I’ve developed over the years:

I fill up an empty Zojirushi water bottle with ice before I leave the house. It’s a very well-insulated flask — over a 24 hour period, the ice barely melts so you can take it through security because it’s not a liquid. Then, you can pour in water later on to melt some of the ice and get a cold drink.

I wear a long sleeved t-shirt onto planes. The cabin gets colder after take off, and it helps not having bare skin exposed to drafts. On the ground, cabins can get pretty warm if you’re somewhere hot and sunny. A light jacket that you have to take off is just one more item you have to juggle, so I prefer just being able to push up my t-shirt sleeves instead. Incidentally, U.S. airlines tend to keep cabins noticeably colder than Asian airlines.

My hands down favorite backpack is the MacPac Korora 16L. It’s compact with well thought-out compartments. There are two deep side pockets so water bottles don’t slip out and an easy-access zipped pocket at the top. Inside the main compartment, there’s a mesh divider and another pocket at the top that has slots for pens and a clip for hanging keys. It easily fits a 14” MacBook Pro in a sleeve, book, and jacket with room to spare. It’s been around the world with me several times — both on work and leisure trips — and has proven to be durable. It’s also water resistant.

I keep a phone charger cable and Airpods in the outside top pocket, and a backup battery and super compact Anker 65W 3-port USB-C + USB-A charger in the side pocket, together with a USB-C cable that has a dongle for converting one end to a lightning connector.

The only thing I would change is to remove the chest strap and buckles that are pretty useless.

We used to avoid checking in luggage if we could help it, but we can now no longer help it. Now we pack a light, empty duffle bag in our suitcase in case we need emergency extra space — such as when encountering a check-in agent that is insistent that the weight limit is 50 lbs and 52 lbs is completely unacceptable.

For the kids, we bought an inflatable footrest. It blows up to fill in the space in the footwell and becomes level with the seat. This lets the two of them sleep side by side across two seats each. When they’re awake, it helps provide a bit of an area to crawl around and reduces the amount of items that drop on the floor. Caution: some airlines don’t permit these because of purported safety reasons (we’ve been successful on American, Fiji Airways, and United, but not Air France).

Further Observations

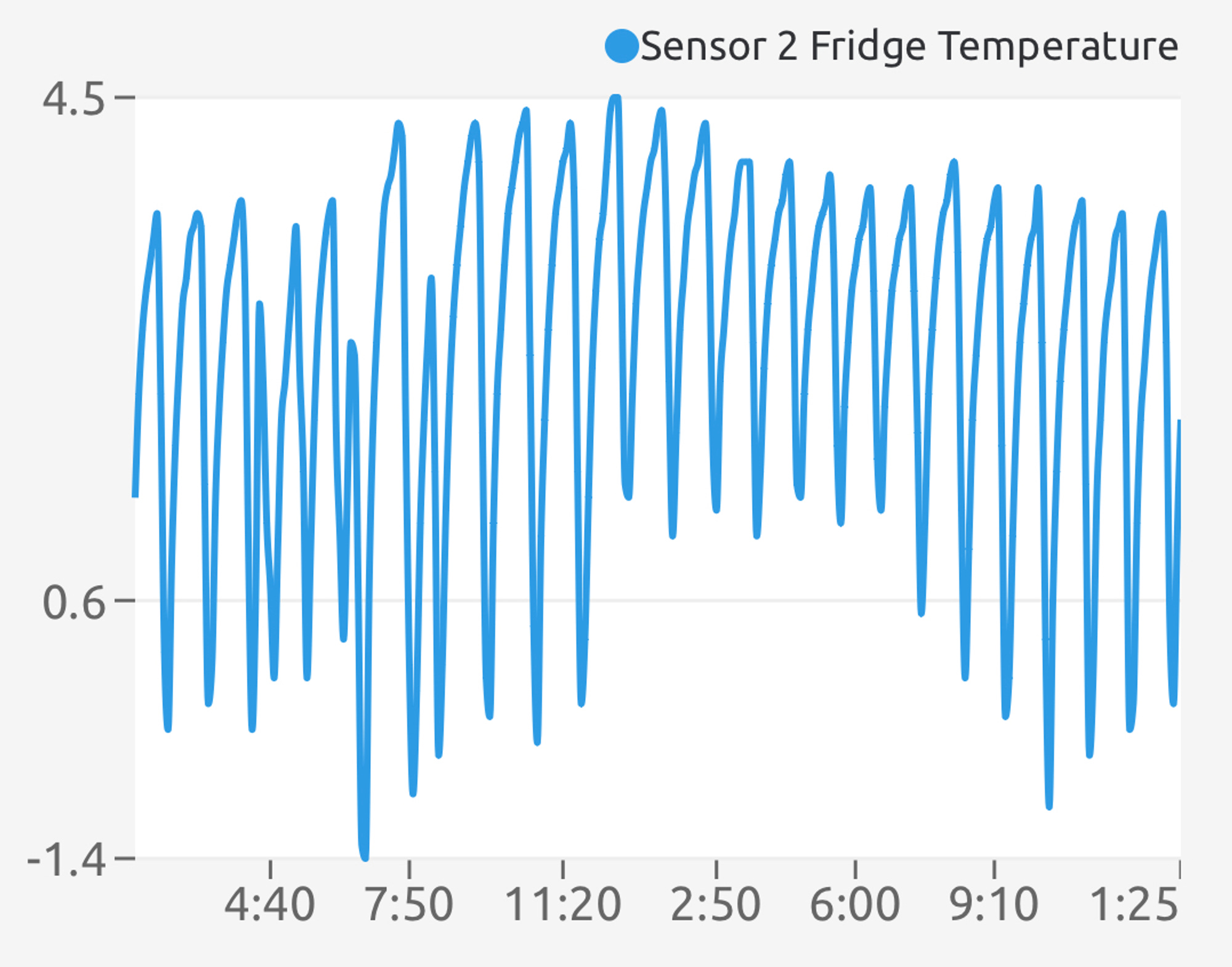

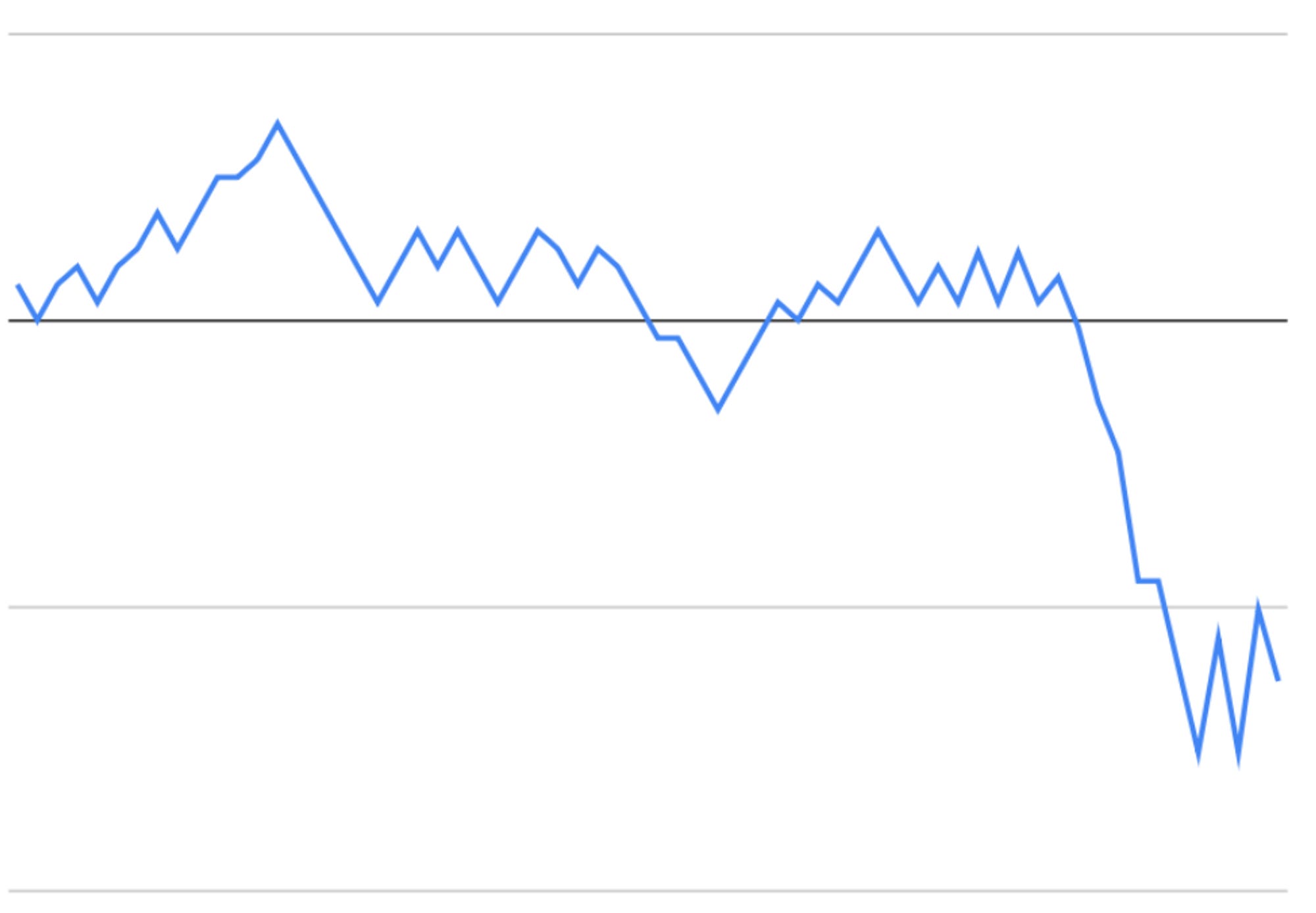

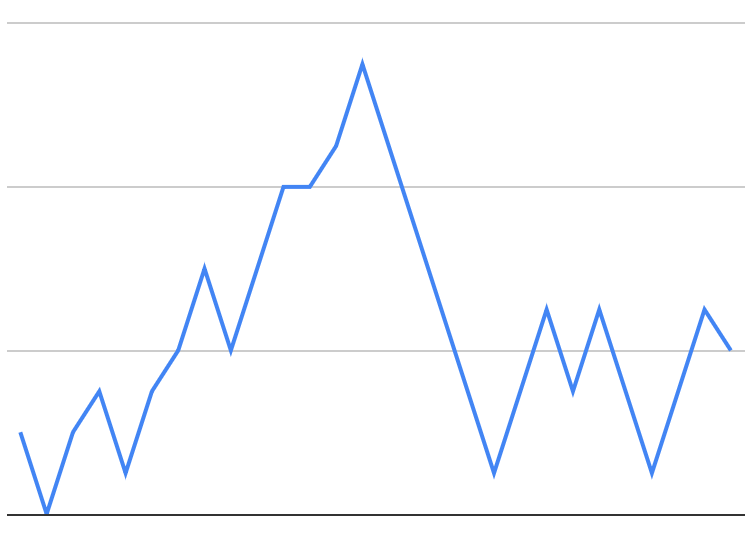

I’ve been eyeing a weather station for years, so I was thrilled when I received an Ambient Weather one as a gift from my family last Christmas. We experience multiple long power outages each year, so I bought a probe thermometer that broadcasts data to the weather station and stuck it in the fridge to monitor the temperature. I figured it would be helpful when we were traveling so we don’t unknowingly come home to a fridge full of spoiled food. The weather station streams the data it collects online and sends text alerts when the temperature reaches certain thresholds (and we have a UPS for our internet equipment so the house stays connected for a couple hours even when the power is out).

Our fridge is set to 2°C and the temperature graph looks like this:

This is not the temperature profile I’d have expected. It never occurred to me that the fridge spends most of its time below 2°C, and sometimes below freezing. However, when you think about it for a minute, that’s the only way it could really work. The fridge doesn’t blow in air at the temperature it’s set at — it blows in really cold air at a fixed temperature and tries to average it out at the set temperature.

I contacted Amazon customer support recently after an order they had marked as having been successfully delivered actually hadn’t been delivered. It got weird:

Regarding the spate of layoffs in tech: what does it really mean when a CEO says they “take full responsibility” for over-hiring? Presumably it means that they are owning making the original decision that caused a bunch of people to then lose their jobs through no fault of their own? But we don’t really hear if there any real accountability or personal consequence to go with that responsibility… And what about the companies that go through multiple layoffs in succession?

We recently returned from a trip to Australia, my first in almost four years and the longest I’ve ever been away from it. It was also my kids’ first visit. Because of the age of our kids and jet lag, we set ourselves a modest goal of doing one thing a day. Apart from family, I only told like, 3 sets of friends that we were visiting Sydney, and even then we only managed to meet up with 2 of them. (Sorry everyone else — maybe next time!)

It was interesting seeing our kids meet their grandparents in person (for the first time ever for one of them), and fun watching them take in the sights of Sydney. Our hotel balcony had a nice view of the overseas passenger terminal at Circular Quay and watching massive cruise liners silently dock enthralled all of us early each morning.

We stayed at a hotel in the CBD for half of the trip, and my parents’ house for the other half. It was nostalgic taking my kids to the parks that I used to play in as a kid. Unfortunately, the one down the street from my parents’ house has been redone twice, each time ostensibly making the playground safer, but decidedly much less fun. Gone is the 3 metre-high straight metal slide, the flying fox, monkey bars, and swings on long chains that I loved to get height on. They have now been replaced with small, boring plastic things.

Sydney continues to grow. Lots of cranes dotted the CBD and the light rail system is now in full operation. We visited Barangaroo and walked through the lobby of the new Crown Casino building. The water park at Darling Harbour was a hit with the kids. Even the Circular Quay skyline has changed. When I used to work in Sydney, for a few months I had loan of a Senior Associate’s office with a thin window on the 57th floor that overlooked the harbour. There was an AMP building between us and the foreshore, but it was less than half the height of our building so the view was unobstructed. In the last couple of years, the AMP building has been extended, doubling in height and it now blocks some of those million dollar views.

For old time’s sake (and because my son loves trains), when relocating to my parents’ house, we took the train — the same route I used to take to and from uni. I felt like an old man reminiscing that back in those days, most of the trains weren’t air-conditioned, and there were no smartphones to occupy the time during the one hour journey.

The trip coincided with Chinese New Year, so we were fortunate to celebrate that with the grandparents and to see some of the festivities in Chinatown (that my daughter had only read about in books up until then).

Fiji

On the way back from Sydney, we experimented with breaking up the flight by stopping over in Fiji for a few days. We decided to stay at Nanuku Resort, mainly because it offered free childcare (one babysitter per child, available from 8am to 8pm!). Also, because it was on the same island as the international airport, we didn’t need to take another plane to get there. (However, the advertised 2 hour drive from the airport turned out to be closer to 3 hours.)

Nanuku is operated by Auberge Resorts, and some of their executives were visiting it when we were there, including its CEO. After finishing up a kayak ride, we bumped into the CEO who took the opportunity to ask why we picked Nanuku (childcare), how we had discovered it (Google + Hyatt partnership), and encourage us — several times — to “come again and tell our friends to visit too” (talk about grassroots marketing!). He asked where we were from, and it turns out that he had grown up in San Mateo (the next city over from us) and was now living in Marin. He happened to be on the same flight as us back to San Francisco. When we joined the immigration line in SFO, our kids were acting up for whatever reason and screaming. He passed us in the queue and joked: ”I bet you wish you were still at Nanuku!”

The staff at Nanuku were all super-friendly and welcoming. Attention to detail was a bit hit and miss, but everyone was well-intentioned which to me counts for a lot. (For example, most staff knew the names of our kids, but it was 50:50 whether they remembered that we needed a high chair at meals for our youngest. There’s only one restaurant on the property.)

The resort had a very relaxed atmosphere, which is exactly what we were looking for. We arrived a couple weeks after peak season, so the resort wasn’t busy and at times it felt empty (which is a good thing at places like these). We overheard the Auberge execs worrying about how occupancy in February was going to be even lower.

They have a decent beach that guests don’t seem to use, and offered a variety of free and paid activities. We (tried to) learn how to start a fire using wood, weave a basket out of a palm frond, and grill prawns using bamboo. We also paddled a kayak down a nearby river, and took a jetski out onto the ocean. Susanne snorkeled out to a nearby reef but the water was too choppy for me (the wind picks up mid-morning so you need to get out early).

We booked partially on Hyatt points (great value at only 30K a night), and partially through the Amex FHR program (which offers discounted rates and a free couples massage). We had a room with a spa out the front and an outdoors shower, which both we and the kids loved.

One of the few resorts where the rooms looked better in real life than the photos!

The flight timings from Fiji back to SFO are good — night departure, long enough to get close to a full night’s rest, and not much filler time on either side. Due to the time zone difference, you land around noon on the same date that you leave.

Further Observations

Going to be interesting to see how the whole affair with Adani turns out.

The Witcher: Blood Origins This 4-episode miniseries was a great way to whet the appetite for the next season of The Witcher, although Henry Cavill’s shoes will be tough to fill. It also stars Michelle Yeoh, who has had a great run as of late (unlike Henry Cavill).

Glass Onion Daniel Craig, playing a southern detective called Benoit Blanc, is a hoot in this thoroughly entertaining whodunnit.

Knives Out This is the first Benoit Blanc movie, but we only watched it after enjoying Glass Onion. Also highly watchable, but not as funny.

Charts, Images & Videos

Pandemic years aside, employment growth is gradual, and unemployment growth is sudden. We haven’t hit the “sudden” part of the current economic cycle yet.

Not a new one— But, I am partial to a good meme, especially when it ties one of my kids’ favorite movie characters together with an aviation factoid. 😄 pic.twitter.com/iqujcGthvc

One thing I miss from Sydney are thunderstorms. It may be a strange thing to miss, but one fond childhood memory I have was of the “southerly buster”. It’s a weather phenomenon that typically happens after a series of hot summer days — the temperature suddenly plummets, huge grey clouds roll in, the rain pelts down, and the sky puts on a dramatic show. I remember gazing out into our backyard as lightning danced in the sky and thunder literally shook the windows. (My father had also drilled it into me that if there was lightning around, I needed to immediately turn off the computer, lest a surge of electricity fry it.)

Thunderstorms don’t really exist in the Bay Area. I’ve been here for almost 15 years and I can count on one hand the number of times I remember hearing thunder. So when the Bay Area experienced a “storm” earlier this week — one that made the national news and saw weather warnings blanket the airwaves — there’s a reason I put storm in quotation marks. To be sure, there was rain and it got quite windy. But, objectively speaking, it was not that wild. I’ve been in rain so heavy that it hurts the skin, and experienced gale force winds that dim the lights. None of those things happened this week in our city. Yet, there was flooding, genuine danger to life, closed schools, and a weather-induced 3-hour blackout in our neighborhood. The Bay Area is just really fragile when it comes to inclement weather.

This week’s 🍿 news story was the vote for the Speakership of the House of Representatives. Kevin McCarthy finally got his gavel, at the cost of selling the last remnants of his soul. Seems like a pyrrhic victory to me, and it’s hard to see it inflicting anything but pain on the country when a small group of Republicans ends up holding everyone else hostage to their demands. And will their brinksmanship turn the prospect a federal debt default from the unthinkable into the possible?

Taking a break, so no newsletter for the next couple of weekends. Will resume in a couple of weeks!

The second shortest travel list since I started making this annual post. But, the good news is that COVID is pretty much over as far as travel restrictions are concerned. 2023 will be more active, based on the travel we already have booked, starting later this month!

San Diego, CA * Copenhagen, Denmark * Paris, France

All places had overnight visits, unless marked with †.

* Multiple entries, non-consecutive days. † Daytrip only. ‡ New country or territory.

Happy 2023! For the last couple of years, I’ve written a Year In Review post that is sent to friends and family. It contains a “What we remember personally” section, which is about personal events, and a “What we remember in the world” section. Below is the latter section from those writings.

The Economy. For the first time in about 13 years, the economy and the markets are deteriorating. For years I’ve believed that inflation was the main thing that was going to catalyze another recession, but I didn’t have a clue what might spark that inflation. At the start of this year, a confluence of factors such as the Ukraine invasion and supply chain shocks, have led to the highest inflation rates in 40 years, which in turn have led to the fastest series of interest rate rises in history.

When interest rates rise, equities become less attractive relative to other assets, and valuations fall. Accordingly, most of the market took a dump, with growth stocks (mostly tech companies) getting hit the worst.

Tech companies, suddenly confronted with an inability to continue raising funds at the same inflated valuations they previously received (or to raise funds at all), were now staring at their runway trying to figure out if they had enough cash to weather the storm. Some laid off employees by the thousands, and the focus moved from growing the top line at all costs, to getting to profitability at the least cost.

However, the market is not the economy, and we have this interesting situation where things feel bad and lots of techies are losing their jobs, but the economy actually isn’t in bad shape just yet. In the U.S. and Australia, for example, unemployment is currently still under 4%, which is pretty much the lowest it’s been for the last 20+ years. A lot of companies are simply reacting before the storm hits. This time, companies are trying to get ahead of it.

I think the real pain of a recession is yet to come. Obviously I could be wrong, but don’t see a soft landing on the cards when the Fed is spamming the interest rate increase button. Sudden changes don’t seem conducive to letting businesses adapt over time to changing conditions, and it presumes that the Fed won’t be late to react again, this time to cooling inflation.

It’s also going to be interesting to see what happens socially and to workplace culture if we do have some sort of economic crisis. The experiences you go through shape your perception of the world, and most people under 33 have not experienced a downturn in their working lives. It’s been halcyon days for a long time. Not knowing any other world, younger workers perhaps have come to take for granted job mobility, a seller’s market for employment, and that dips in the market are simply short-lived buying opportunities.

I have been through two economic downturns — graduating at the nadir of the dot com crash in the 2002, and again during the GFC in 2009. In 2009, the job market had completely dried up and I was proofreading documents for $13/hour and trawling for contract jobs on Craigslist (I actually found a couple) to make ends meet and try to maintain my U.S. visa status. I was down to about $600 in my bank account at one stage, sharing a 2-bedroom apartment with 3 other people. I always had a backup plan — returning to Australia and a job that I had taken a 3-year leave of absence from — but through that experience, I know how tough things can get in bad times and sometimes you just have to leave your ego at the door.

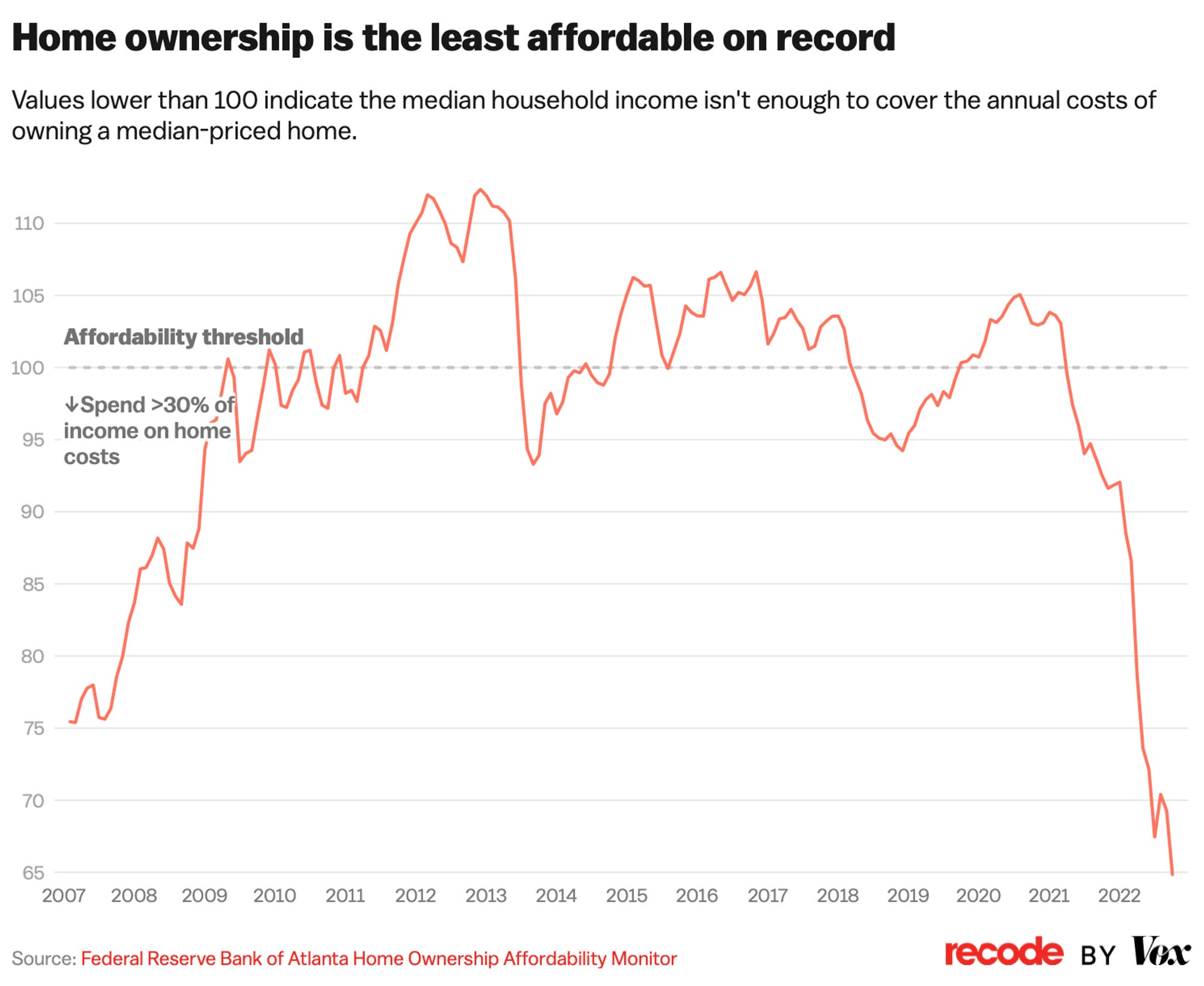

Housing affordability is another problem, and one problem has been swapped for another: record low interest rates pushed housing prices through the roof, making deposits difficult to afford for younger millennials and Gen Z. Now higher interest rates are pushing interest payments through the roof, while housing prices are still very elevated.

One thing this indicates is that there is no end in sight for the growing economic inequality between younger and older generations. I don’t know what this means exactly, but the trend is unsustainable and will eventually end in trouble if not reversed.

Roe v. Wade was overturned by Dobbs. In June, a precedent that stood for almost 50 years was overturned by the Supreme Court. The ruling split 6–3 along ideological lines (some would say party lines). It is impossible to overstate how deeply the court’s composition has and could impact the fabric of American society over the next generation. Let’s just say that for now we are relieved we live in California, but it’s a reminder of how quickly things can shift. Also, Ketanji Brown Jackson was appointed to the Supreme Court.

AI. One of the most notable technological developments in a while is the raft of consumer-accessible AI software that gained prominence this year: ChatGPT, DALL•E 2, Stable Diffusion, Midjourney, Jasper, Lensa, Notion AI, etc. Unlike web3 or the Metaverse, which are solutions in search of a problem, the utility and impact of these forms of AI are immediately understandable. I think these technologies will make the biggest impact on society since the shift from desktop to mobile a decade ago. The tech is already pretty eye-opening, and OpenAI is still to release GPT-4, which is rumored to be a couple orders of magnitude more powerful.

Queen Elizabeth II died on September 8, 2022. She was such a fixture in the world that it still feels weird that she’s gone and we have a King Charles III. Oh, and Liz Truss’ short reign as PM is kind of a footnote to this event. My wife points out that, remarkably, her Queen Margrethe is now the world’s only current female monarch. Margrethe II celebrated her golden jubilee (50 years on the throne) this year.

Scomo was voted out. In May, Australia held an election and voted Scott Morrison out. Not sad to see the departure of Scotty from Marketing who left his mark in Engadine.

Xi Jinping was elected to a new 5 year term. Xi Jinping was elected to an unprecedented third 5-year term, solidifying his autocratic grasp on power. However, cracks are starting to take their toll on China. One of the sad casualties through all this has been Hong Kong, which now seems like a shell of its former vibrant self.

November mid-term elections. I called this one wrong last year. I thought it would be a landslide, but it wasn’t and the Democrats even expanded their control of the Senate. The results gave us some hope here that Trumpism is on the wane. It was also the first U.S. federal election that I voted in.

The Metaverse. Lots of coverage about this, but I don’t see anyone of any generation scrambling to get on board the metaverse train. If there is a metaverse that takes traction, it ain’t going to be Meta’s — my prediction is that it will come from a gaming company. (Scott Galloway on the ~$1B a month Meta is spending: “Instead, spend the money on employee retention, and every workday at HQ raffle off an Airbus A380 (resale value: $50 million) to a lucky employee.” A380s are more expensive than that, but the underlying point is still valid.)

Elon Musk & Twitter. A morbidly entertaining saga. It will be interesting to see what comes of Twitter in 2023. Things are so random it’s tough to make a prediction here, but I don’t think Twitter is getting back to its $44B valuation in the next 5 years (if ever).

FTX blew up. I’ve written about this at length, but it’s been another morbidly entertaining story. I can’t wait to read Michael Lewis’ book and watch the movie.

Crypto winter. This year, the get rich quick scheme that perhaps many recent participants in the market hoped to capitalize on turned into a get poor quick scheme. I believe crypto is correlated with the larger market, and it will largely move in line with what happens to the economy next year (just more violently). And hopefully the sector picks up some regulation to protect more consumers from losing their shirts to bad actors.

Uvalde School Shooting. In America’s third deadliest school shooting, 19 students and 2 teachers died while police controversially waited for over an hour to engage the shooter, instead confronting parents who were trying to get in and save their kids.

Shinzo Abe was assassinated. Assassinations are always jarring news.

J-Lo and Ben Affleck got married. Not much to say here, but this was one of the main things Susie said she remembered from the year! Will Smith slapping Chris Rock at the Oscars, and Johnny Depp winning his defamation case against Amber Heard, rounds up other memorable celebrity events.

The Cosmic Cliffs, a region on the edge of the gigantic, gaseous Carina Nebula, as seen by Webb’s Near-Infrared Camera. Source: NASA, ESA, CSA, STScI

A close-up of the star Earendel (red arrow). At a co-moving distance of 28 billion light years, it’s the most distant individual star ever seen. Source: NASA/ESA/CSA/STScI

On Twitter

This runner exited a train, ran to the next stop, on got back on the same train pic.twitter.com/mk8PPynVqa

Merry Christmas! I hope you are enjoying a nice long holiday weekend with your friends and family. Just a short update this week. Next week I’m planning to do a Year In Review.

Sam Bankman-Fried is hosed. Earlier this week, he agreed to be extradited back to the States. Bail was set at $250M, which means that anyone who’s willing to post bail for him (i.e. his parents) will basically be bankrupted if he skips town. His co-founder Gary Wang and Alameda CEO Caroline Ellison both pleaded guilty to various criminal counts and are cooperating with authorities in their criminal and civil cases against SBF. More of his former associates are expected to flip. Hard to see how he doesn’t get put away for a long time.

Frozen: The Musical. We took our daughter to see this at the Orpheum (her first musical!). Frozen is a phenomenon and not easy source material to adapt for the stage, so I was curious to see how it would play out. The result is a musical that shines at moments, but otherwise lacks the dynamism of its animated compatriot. There are a variety of new songs that were created just for the musical (written by the original music writers), but none of them were memorable. It all felt like filler music, lacking any tunes that really catch. The performance of a new song called Hygge stuck in my mind, but I can’t recall the melody at all.

The most authentic response was probably looking at how our daughter reacted. Like probably every other child (and parent) in the audience, she has watched Frozen dozens of times, and has made us play the soundtrack in the car at least several hundred times (I have the Spotify stats to back that up). Our daughter was completely enthralled with the major set pieces: Do you want to build a snowman?, For the first time in forever, Love is an open door and, of course, Let it go. The way young Elsa and Anna were portrayed were a delight. But Frozenfront-loads all its big musical pieces, and as the second half dives deeper into a darker story, her attention started to wander. She seemed bored with the new songs and I wonder what was going through her mind when they replaced the cute rotund trolls with “hidden folk” — essentially wildlings in rags. I think they did the best that they could, but the movie is a tough act to follow!

Trivia: Frozen is set in Norway, but the movie’s is loosely based around Danish author Hans Christian Andersen’s The Snow Queen (Snedronningen).

Well that happened fast. Sam Bankman-Fried was arrested on Monday, the day after he said in a Twitter Space session, “I don’t think I’ll be arrested.” He’s been criminally indicted and slapped with a civil suit and he’s now being held in a nasty ass Bahamian prison awaiting extradition. Cluelessness or arrogance? How about both.

The World Cup is now over and what a final! It was a really enjoyable tournament with lots of memorable upsets (including, finally, one for Australia!) and a fairy tale ending for Argentina and Lionel Messi. Mbappe is only 23 and already has 12 world cup goals. Next time: The World Cup comes to North America!

Fantasy League final result: ended up squarely in the middle of pack, 7 out of 14. Some learnings:

It’s harder to get ahead in the late stages. People end up picking the same players and it’s clearer which players are in good form.

Have to keep on top of injuries in the late stages; it’s a long campaign and it takes its toll.

Making opinionated, defensive bets where you stack the defensive line with a single country is a high risk strategy, but it can work as a hail mary if you’re lagging.

Head-to-head betting final result: a big run during the early knockout stages put me deep in the black. Also, we have extra bets for penalty kicks and I ended up on the right side of all 5 of them (incidentally, that’s the most PKs in World Cup history).

Lower = better for me

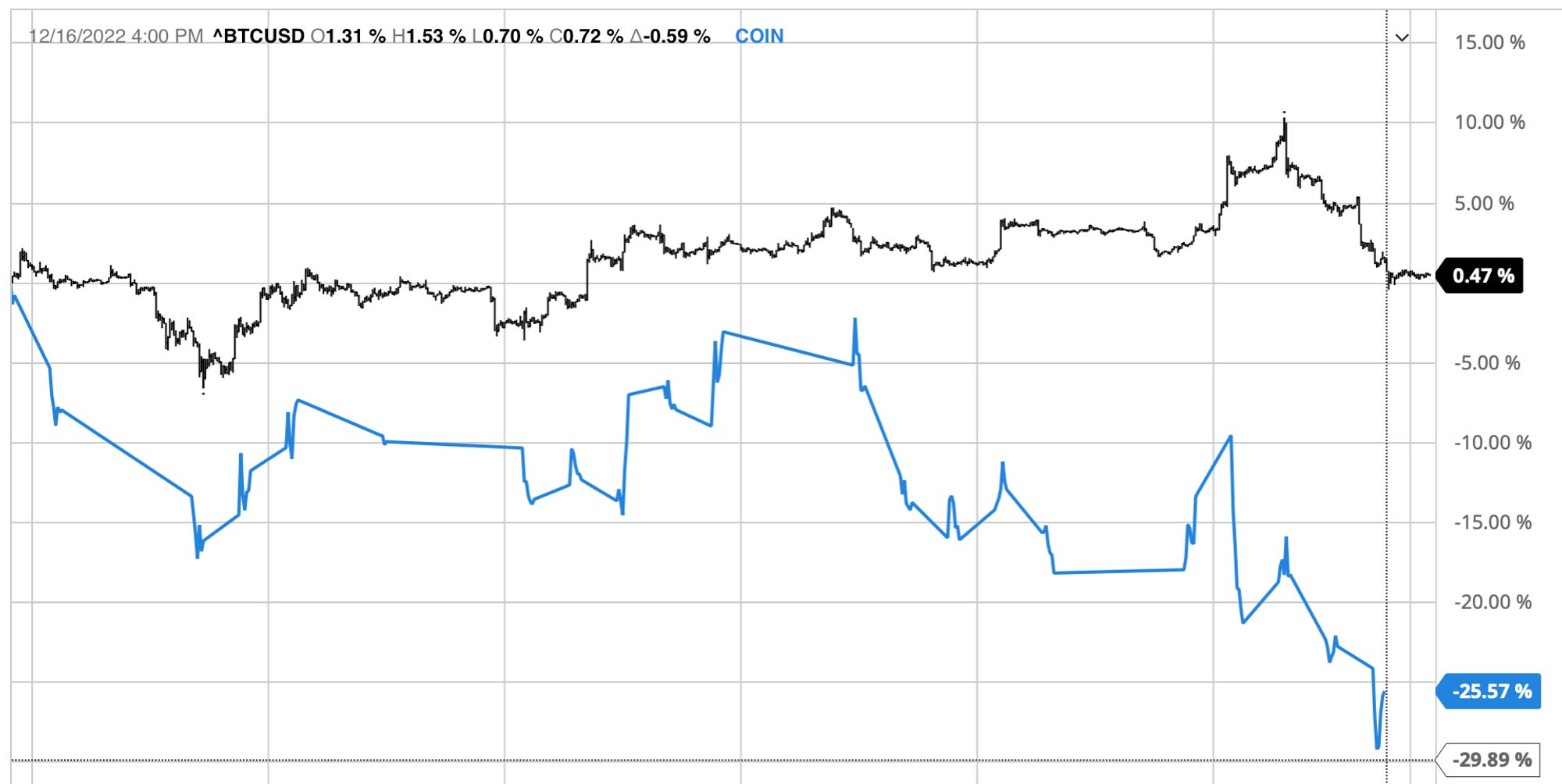

Active week for financial data. The Fed raised rates by 50bps as the market expected, and Powell gave guidance that they are not done with rate rises (also expected). CPI came in at 7.1%, down from 7.7% last month, and under the 7.3% expected by the market. The market closed the week lower. Bitcoin has been relatively stable, but despite that, Coinbase stock has been smashed.

Scientists, for the first time, have created a net energy output from a nuclear fusion reaction. I’m not sure if it will happen in my lifetime — fusion research has been happening long since before I was born — but if they crack it and then make it economical, it’ll revolutionize the world and probably go a long way towards solving climate change.